Why this matters: Real estate agents and brokers in 2025 observed a disappointing spring sales bounce after years of substandard home sales since the 2021 pandemic buying frenzy. Buyers lost purchasing power to the highest mortgage rates and asking prices since 2013 and have backed off from buying. In turn, inventories of property for sale have and will continue to pile up with a vengeance – until sellers drop asking prices or get out of the market.

Current home sales to depleted buyers

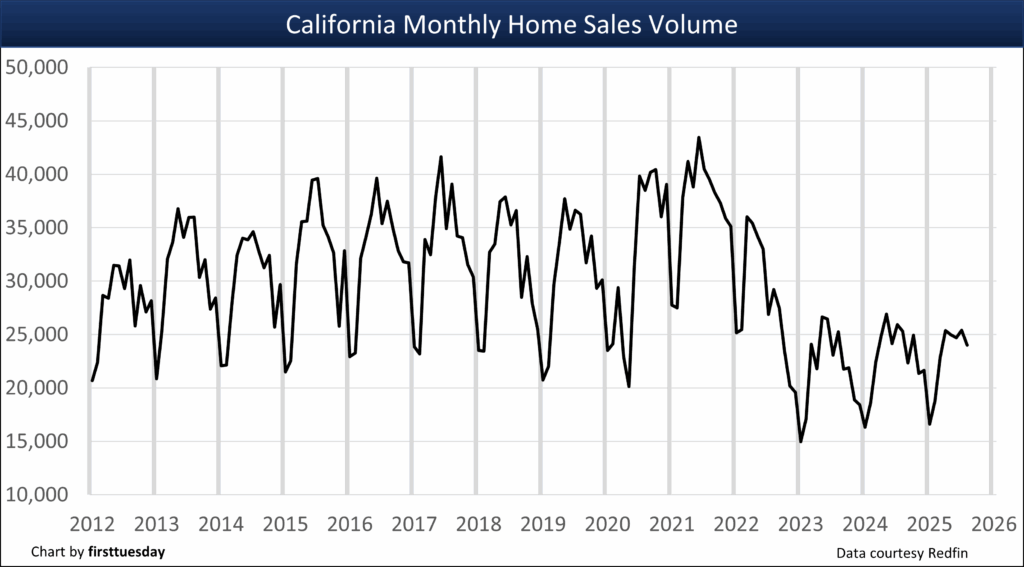

In August 2025, California saw 24,000 escrows close for new and resale home transactions. Sales volume in August dropped 5.2% below the same month one year earlier.

Importantly for trends, year-to-date (YTD) sales volume through August 2025 only declined 1.0% from the 2024 YTD sales figure. The significant decline in August sales volume from earlier months suggests the buyer retreat has accelerated since the anemic spring bounce.

Compared to 2019 — the last normal year before the economic tsunami of the 2020 pandemic — 2025 sales volume YTD is trending at least 34% lower. A real estate recession by any standard, the pandemic years being a period of financial anomalies.

Recent home sales trends

Consider that annual home sales experienced a 6% bounce from 2023 to 2024. More critically, sales volume in 2024 was 27% below 2019 — the last year in the past sales cycle.

Understand that the homebuyers available for 2023 were cannibalized in 2021 by incentives in the pandemic-driven buying spree. Today, buyers are waiting until they sense the decline in pricing is over, evidenced when prices bottom and begin to rise. Be aware your typical homebuyer today knows their math for income-to-mortgage leveraging to set home pricing, thanks to readily available insight.

The developing public uncertainty about political upheaval, trade taxes and immigration hostilities dampens down owner and tenant turnover, and thus sales volume. The property sales market will suffer from this rigor mortis until speculators turn to the real estate market and stop prices from dropping.

Today’s sales volume strikes at pricing

Watch for home sales volume to further trail off by the end of 2025, as the seasonal dip combines with buyer caution around increasingly troubling employment conditions.

When home prices decline across all pricing tiers, not just the high tier now underway, recent homeowners with little down payment can only watch as the equity in their home slides underwater. This pricing-to-mortgage crossover event is not likely to begin until a nationwide economic recession brings on a further drop in the number of Californians employed. Also, keep an eye on the slow upward trend from very low rates of mortgage foreclosures as a force compelling owners to sell in the future.

Sales agents can expect the current real estate recession to eventually bring about a return of real estate speculators after prices drop to produce a “dead cat” bounce in both sales volume and pricing. Within 12 months following the speculator-driven market bounce, home prices historically slip as homebuyers wait and watch before prices bottom that year. It is then that a sustainable sales volume and pricing recovery takes over with the return of end-user homebuyers – and temporarily lower mortgage rates.

Updated September 2025.

Chart 1

Chart update 9/24/25

Aug 2025

Aug 2024

YoY change

California home sales volume

24,000

25,300

-5.2%

Home sales fluctuate from month to month for a variety of reasons, all worth an agent taking time to consider them. The most significant reason is the volatility of homebuyer demand. Several factors constantly at work moving the California homebuying market including:

Seasonal differences in annual sales volume

It’s normal for home sales volume to rise in the first half of the year and fall after peaking around June.

Chart 2

Chart 2 shows average home sales volume experienced from 2011-2018, the recovery period following the Great Recession. As depicted, the month with the most homes sold monthly during a year close escrow in June. Another upturn takes place in December, as homebuyers seek to wrap up their financial activities before the end of the year.

Real estate agents need not fuss when they hear of falling month-to-month sales volume in the latter half of the year. It is the normal cycle of seasonal progression taking place. What to watch for is year-over sales, to compare recent months this year to the same months last year or compare another period such as year-to-date to best see a trend.

As a rule, current market activity, whether up or down, is reflected first in sales volume, followed in nine to 12 months by price adjustments in the same direction.

Chart 3

Chart update 9/24/25

2025 Forecast2024

2023Annual changeAnnual home sales volume265,300274,550260,200+5.5%

To set the stage for a forward look, a review of sales volume in the recent past is helpful:

2018 saw sales volume decrease rapidly in the fourth quarter, ending the year 4% below 2017;2019 home sales volume decreased slightly from the prior year as we headed into the 2020 recession;2022 home sales volume peaked early in March and lost all ground gained in the pandemic year of 2021, ending the year 24% below 2021, but only 12% below 2019, the last “normal” year for home sales before the pandemic upended market dynamics;2023 home sales volume lost a further 22% over the prior year, the further result of buyers pulled forward to buy in 2021 using historically low mortgage rates for funding;2024 home sales stabilized from the prior year, suggesting the end of the ripple effect from pandemic economics; and2025 continues the stagnant sales trend of the prior two years, as forecast in the dashed column above.

Chart 4

Chart update 9/24/25

Aug 2025Aug 2024Aug 2023Home sales volume

year-to-date

182,600184,600179,300

Year-to-date (YTD) home sales volume through August 2025 was substantially the same as the year prior. As of August 2025, YTD home sales volume is 1.0% below a year earlier. Compared to 2019 (the last “normal” year for housing before the pandemic economy took over), home sales volume YTD is 27% lower in 2025 as of August. The present monthly trend in sales volume is even lower going into 2026.

Home sales volume continues a slow decline in 2025, due to:

the real estate recession, yet to be declared, but three years underway throughout California;high mortgage rates reducing homebuyer ability to pay seller asking prices;buyer agent failure to advise buyers who signed a representation agreement to disregard asking prices and make offers at prices they qualify to pay;reluctance of home sellers to reduce asking prices to offset high mortgage rates;a rapidly increasing home inventory available for sale across the state causing buyers to wait; anda consistent quantity of all-cash buyers undeterred by interest rates or asking prices.

Home sales in the coming years

The forward trend in California home sales is one of caution and delay for both buyers and sellers. Homebuyer income is growing but only keeping up with inflation, much improved from the less-than-inflation pace during the decade preceding the pandemic.

However, wage increases were not enough to catch up much less keep up with rising house prices, still far above the mean price trendline. The upcoming necessary price adjustment will be especially resisted by sellers’ pricing stubbornness, known as the sticky pricing phenomenon. Many sellers in a devalued real estate market which mandates a reset of asking prices will withdraw their property from the inventory available for sale when prices trend lower.

firsttuesday forecasts annual home sales volume will slip around 3.5% in 2025, and that the slipping will accelerate come 2026. The decline is the result of the tandem high levels of both asking prices and mortgage rates. One or the other, but not both can rise vertically as buyers then become far less able to buy. In essence, sellers today complete with rents charged by landlords and interest charged by MLOs.

The timeline for a real estate turnaround is faced with additional complications not experienced in recent decades. Government trade wars are raising the cost of domestic and imported materials which are compounded by the federal attack on the necessary migratory labor force for construction and maintenance of a home and household. Additionally, these complications are a broadly based interference with our keeping the California economy the fourth largest in the world.

The competitive broker

What’s a broker reliant on home sales to do until home sales volume provides abundance again?

SFR brokers and agents might consider adding transaction-related services to supplement their income in the present buyer’s market. Those who do add related services, provided only when the client signs a representation agreement, will restructure their practice as “all-service brokers.” Transaction-related services typically originate with representing buyers, and when integrated into an office operation help maintain their agents’ standard of living, remain solvent and position the office for eventual growth.

Related video:

Introducing the Buyer Representation Agreement

The trend in California home sales during the initial years of the 2010s remains grim for sellers. Not so for buyers. Homebuyers’ dollars are going further than anytime during the past 15 years.

Sales now and into 2014 will remain excessively lender-driven and speculator-riddled, but will be easily predictable for SFR agents and their brokers. The center of this action is the multiple listing service (MLS).

To set the stage for a forward look, a review of sales volume in the recent past is needed:

Mid-2005 saw sales volume peak for all types of real estate in California;Early 2006 produced both the peak in sales prices and the initial precipitous decline in sales volume. Nearly 30% fewer sales were recorded in 2006 than in 2005;In 2007 sales volume dropped another 30%;2009 sales were artificially higher than anticipated due to subsidy-induced purchases and speculators, but remained 40% below the 2005 peak year;2010 saw a decline from the year earlier in both sales volume and prices;2011 increased slightly in sales volume while decreasing in sales prices; and2012 saw sales volume and home prices increase marginally, supported primarily by massive speculation.

Related articles:

California tiered home pricing

Budging from sticky pricing (or not).

Real estate owned property (REO) resales and speculators have contributed to sales volume oddities over the past few years. Conventional positive equity sales remain the exception.

Lenders have turned increasingly to short sales in 2012, surpassing the number of foreclosures in California. Short sales will continue to make up roughly one-fourth of the home resale market in 2013.

Going into 2013, sales volume is gradually recovering as speculators begin to exit the market, making room for buyer-occupants.

Sales volume will likely increase by 10% in 2013, due to slowly improving confidence and job numbers. Anticipate modest price increases to follow in 2014, falling back in 2016.

In 2015, the Federal Reserve (the Fed) will need to raise short-term interest rates in order to keep a lid on the recovery (as they did in both 1984 and 1994). Expect the short-term rate to decline within one year, the 2016 period, at the end of a downward turn in real estate sales volume.

Sales volume’s next big peak will occur in 2019-2020, with pricing following 12 months later.

Related article:

Suspect behavior: why and how the Fed creates a recession

The real estate market is now settling into a long recovery.

For home sales volume to achieve the kind of dramatic but stable recovery which took place in the 1996 period following the 1990s real estate recession, employment will need to increase at the rates experienced in the mid-1990s: 350,000+ additional jobs created annually for three years. California’s labor force is inching back to that number, as a total of 700,400 jobs have been gained since employment was at its lowest in January 2010. However, as of October 2012, California is still 900,000 jobs short of the employment level before the Great Recession.

Once Californians feel the effects of two or three years of healthy employment growth, their confidence about the future will improve. They will once again be willing to invest in the economy. Only then will end users return in sufficient numbers for sales volume to swell.

Related article:

Homebuyers feel ready and willing to buy, but not financially able

In 2017, sales volume will begin to pick up significantly, peaking in 2019-2020. Employment will have reached its 2007 peak, and will continue to grow quickly. 2017 will see home prices jump well beyond the rate of consumer inflation.Mortgage lenders with an eye for profits will then begin to loosen their lending standards to whatever extent federal regulators permit. The memory of the grim mid-2000s will be quickly pushed aside, and mistakes will be repeated.

Beginning in 2016-2017, another wave of investors and an upsurge of household formations by first-time homebuyers, will kick-start sales volume. In turn, this will drive pricing momentum upward once again. Keep your eyes on homebuyer demand (not sellers, median prices or the MLS inventory). Real demand is driven by:

age demographics;interest rates;tax credits;new jobs; andrising real estate prices.

Related article:

It’s the demand, stupid!

Many favorable market factors are currently support increasing sales volume:

a slow (but steady) increase in the number of new jobs;direct lender subsidies from the federal government for loan modifications on upside-down mortgages;much lower high-tier home prices (as well as more price declines in low- and mid-tier homes), stabilizing in 2013;no major increase in new housing starts into 2014 beyond 10-12% annually;increased short sales;slowly rising consumer confidence and spending; andthe recapitalization of the private mortgage insurers to eventually replace government guarantees of home mortgages.

However, many unfavorable market conditions restrain the rise of home sales volume:

deflationary pressure on consumer and real estate prices (labor, materials and the price of land have become less expensive);the high level of underwater homeowners in California, who will not collectively reach solvency until 2025;the weakest homebuyer demographics in 15 years;the public’s increasingly anti-business and pessimistic attitude about American economics; andtightened loan standards as lenders are forced to apply the forgotten fundamentals of sound mortgage lending practices (20% down payment on all non-FHA loans, lower income ratios, risk-free credit scores and full documentation of income and funds).

What’s a broker to do until home sales volume takes off?

SFR brokers and agents can consider adding SFR-related services to supplement their income. Those that do add related services will restructure their practice as all-service brokers. Transaction-related services will be integrated into their office operations to remain solvent and grow.

These services include:

escrowing their in-house transactions under the broker’s license;entering into or expanding property management services;inspecting vacant homes and issuing broker price opinions (BPOs) for REO lenders as foreclosures increase around 2016;negotiating equity purchases for investors from sellers-in-foreclosure who have a positive equity or the chance of a short sale discount;specializing in sales and leasing of a particular type of commercial property, other branch locations and alternative marketing approaches;providing mortgage loan broker services for business-investor loans made by private lenders (no mortgage loan origination (MLO) endorsement required);arranging carryback financing and loan assumptions, and buying and selling those carrybacks;negotiating options to buy;exchanging properties with equities to help owners relocate their wealth held in real estate; orusing barter credits in lieu of greenbacks, etc.

Brokers can also insist that prospective buyers commit to exclusive representations by a broker and agent to locate a home (or other property). By signing an exclusive right-to-buy listing agreement, buyers are asked to employ brokers and agents just as sellers are asked to employ listing agents. This will ensure time spent with a buyer produces a closing and a fee.