The Typical Buyer & Home Bought

In this section, we provide a high-level overview of key buyer information and what their homes look like. According to the Census Bureau American Community Survey (ACS), 5% of adults in the country are recent buyers. Throughout this section, information about buyers comes from CHTR, and information about other groups comes from ZG Population Science analyzes using ACS data.

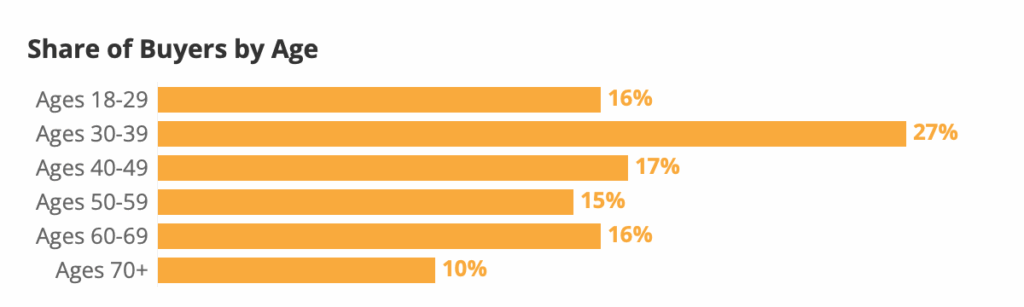

Age

The median age of U.S. buyers is 42, while the average skews higher (44 years old). About one in five buyers (21%) are in their twenties or younger and roughly a fifth (20%) are in their sixties or older.

Age Group

Successful Buyers

Household Decision Makers

US Adults

Ages 18-29

16%

11%

20%

Ages 30-39

27%

18%

18%

Ages 40-49

17%

17%

16%

Ages 50-59

15%

17%

16%

Ages 60-69

16%

18%

16%

Ages 70+

10%

20%

15%

Source: Household decision maker and US adult estimates from Census Bureau, 2024 Current Population Survey Annual Social and Economic Supplement

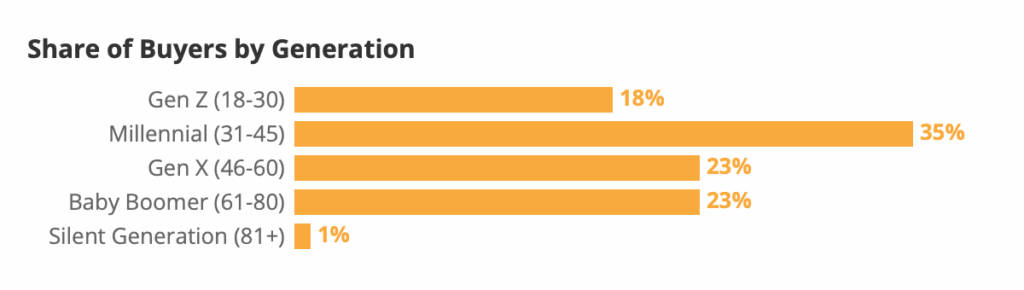

Generation1

Buyers

Household Decision Makers

US Adults

Gen Z (18-30)

18%

11%

20%

Millennial (31-45)

35%

26%

26%

Gen X (46-60)

23%

25%

23%

Baby Boomer (61-80)

23%

31%

26%

Silent Generation (81+)

1%

7%

5%

Source: Household decision maker and US adult estimates from Census Bureau, 2024 Current Population Survey Annual Social and Economic Supplement

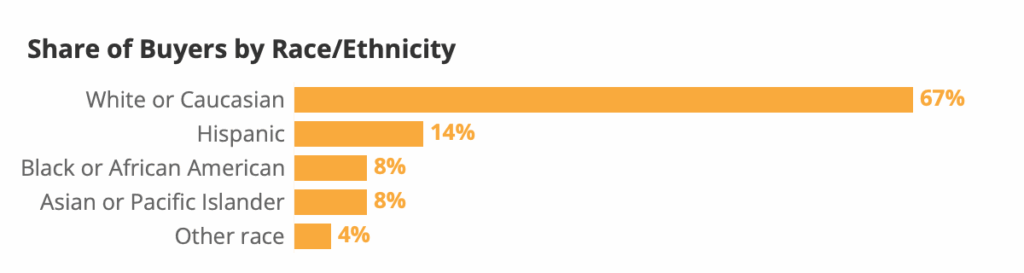

Race & Ethnicity

About two thirds of buyers are non-Hispanic white or Caucasian (66%), higher than the overall share of the U.S. adult population that is white (60%). At the same time, 18% of U.S. adults identify as non-Hispanic Black or African American, but just 9% of buyers are Black.

Race & Ethnicity

Buyers

Household Decision Makers

US Adults

White or Caucasian

67%

63%

60%

Hispanic

14%

12%

12%

Black or African American

8%

15%

18%

Asian or Pacific Islander

8%

6%

6%

Other race

4%

4%

5%

Source: Household decision maker and US adult estimates from Census Bureau, 2023 American Community Survey

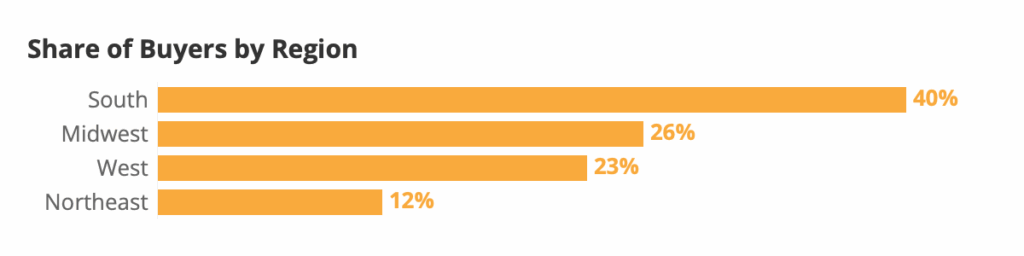

Region

The largest share of buyers live in the South (43%), followed by the Midwest (23%) and West (21%). The smallest share lives in the Northeast (13%). Buyers largely follow the distribution of US adults, with a higher concentration in the South – the region with the most home construction and inventory.

The table below also compares this distribution of buyers by region with the distribution of for-sale inventory that we see on our site. Consistent with the graph above, the South has the most for-sale inventory, while the Northeast has the least.

Region

Buyers

Household Decision Makers

US Adults

For Sale Housing Inventory

Inventory (Field Period)

South

40%

39%

39%

55%

54%

West

23%

22%

24%

20%

19%

Midwest

26%

21%

20%

15%

15%

Northeast

12%

17%

17%

10%

12%

Source: Household decision maker and US adult estimates from Census Bureau, 2023 Current Population Survey Annual Social and Economic Supplement Share of For Sale Housing Inventory comes from Zillow’s listings data as of July 11th, 2024.

Gender Identity & Sexual Orientation

Approximately 10% of buyers identified as LGBTQ+ in 2025

The percentage of buyers identifying as LGBTQ+ has been relatively stable over the last few years. About one in fourteen (7%) buyers identified as LGBTQ+ in 2019, the first year CHTR asked about sexual orientation and gender identity, then 9% in 2020 and in 2023.2 This likely represents the growing share of younger buyers, who may be more likely to feel comfortable self-identifying as LGBTQ+.

Buyers that identified as LGBTQ+

2019

2020

2021

2022

2023

2024

2025

7%

9%

12%

10%

9%

11%

10%

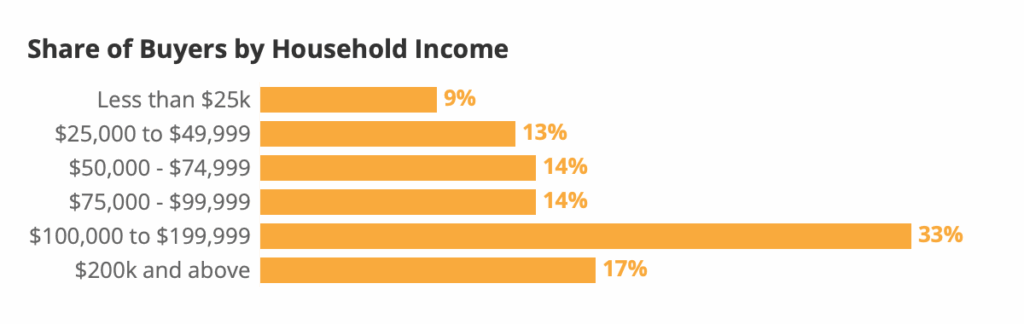

Income

Unsurprisingly, buyers tend to have higher household incomes than the U.S. population overall. The annual median household income among buyers is approximately $97,600, compared to the overall national median of $74,600.3

Income

Buyer Households

All US Households

Less than $25k

9%

14%

$25,000 to $49,999

13%

17%

$50,000 – $74,999

14%

16%

$75,000 – $99,999

14%

12%

$100,000 to $199,999

33%

26%

$200k and above

17%

14%

Source: All US household estimates from Census Bureau, 2024 Current Population Survey Annual Social and Economic Supplement

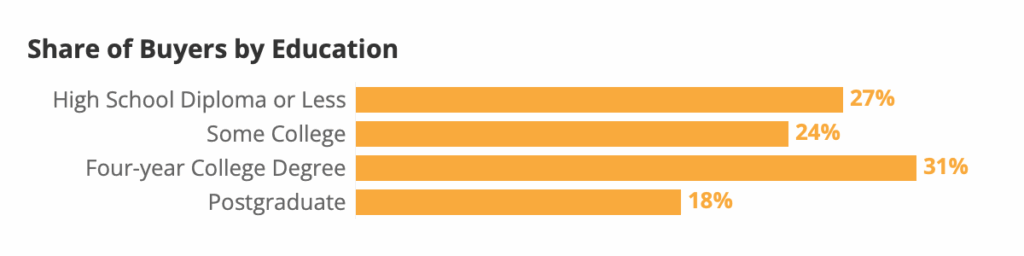

Education

Buyers tend to be more educated than the overall population of U.S. adults: 49% of buyers have at least a four-year degree, higher than 35% of overall U.S. adults.

Education

Buyers

Household Decision Makers

US Adults

High School Diploma or Less

27%

34%

38%

Some College

24%

27%

26%

Four-year College Degree

31%

24%

22%

Postgraduate

18%

15%

13%

Source: All household estimates from Census Bureau, 2024 Current Population Survey Annual Social and Economic Supplement

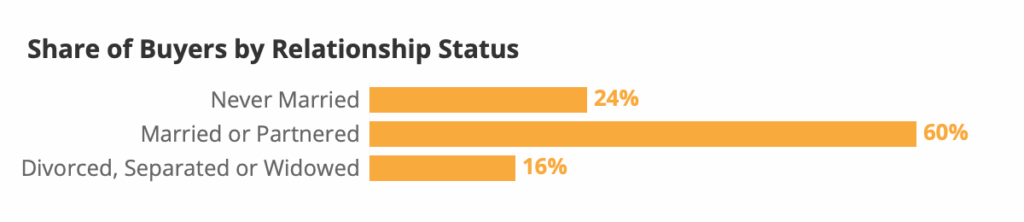

Relationship Status

Prior research has shown that the purchase of a home is often tied to family formation or other life events, like a divorce or separation. This relationship between homeownership and family formation helps explain why over two thirds of buyers are married/partnered (70%) and almost a sixth (15%) have been married in the past.

Relationship Status

Buyers

Household Decision Makers

US Adults

Never Married

24%

18%

28%

Married or Partnered

60%

59%

55%

Divorced, Separated or Widowed

16%

23%

17%

Source: All household estimates from Census Bureau, 2023 Current Population Survey Annual Social and Economic Supplement

Household Composition4

Buyer households are more likely to report having at least one pet (76%) than a child (43%). Dogs are the most common pet among buyer households (64% report having at least one) followed by cats (42%).

In Household

Buyer Households

Tenured Homeowner Households

All Households5

Children under 186

36%

44%

43%

Plant

62%

–

–

Dog

64%

46%

38%

Cat

42%

34%

22%

Another pet

12%

10%

10%

NET: Any pet

76%

61%

50%

The shopping journey takes various paths, but usually starts with an agent

Agent contact usually comes first

When asked about the order they completed homebuying tasks, the most common first step was contacting a real estate agent (52%). 80% of buyers reported contacting an agent as their 1st, 2nd or 3rd homebuying activity.

1st

2nd

3rd

First 3

Contact a real estate agent, realtor or broker

52%

12%

16%

80%

Contact a mortgage lender

18%

19%

16%

53%

Get pre-approved for a mortgage

14%

26%

16%

55%

Attend an open house

8%

10%

10%

27%

Buy homeowner’s insurance

5%

6%

4%

15%

Take a private, in-person tour of a home

4%

28%

23%

55%

Made an offer on a home

0%

0%

12%

13%

A smaller share (18%) said that contacting a mortgage lender was their first step – 53% said contacting a lender was among their first 3 steps. Similarly, 55% of buyers said they got pre-approved for a mortgage within their first 3 steps – but only 14% said it was their first activity.

Of the most common buyer activity sequences, buyers were more likely to start with contacting an agent (39%) than contacting a lender (13%) or getting pre-approved (5%).

Buyers’ most common second step was taking a private, in-person home tour (28%). About half (51%) report such a private tour as their 2nd or 3rd step. A near-unanimous 94% of buyers said that a real estate agent or someone from their brokerage firm helped them access and tour for-sale properties at least once.

Agents were also the most common way that buyers reported finding an open house (58%) – higher than real estate websites (35%) like Zillow.

Most buyers installed a real estate app

Most buyers (79%) reported installing a real estate app during the homebuying process. Among this app-installing group, 86% reported installing before the other steps we asked about (e.g. contacting an agent, lender, touring, pre-approval, etc).

As of completing the survey, most buyers that installed such an app said they never uninstalled it (55%) while a third (36%) said they uninstalled after buying their home. Only 9% of app-installers reported uninstalling before they finished their home purchase.

60% report homebuying stress

About 60% of buyers said that their experience buying a home was at least somewhat stressful. About a quarter (25%) said it was very or extremely stressful.

Homebuying stress

Total

First- time

Repeat

Very/extremely stressful

25%

31%

19%

At least somewhat stressful

60%

66%

56%

Not very/at all stressful

40%

34%

44%

First-time buyers consistently reported higher levels of stress compared to repeat buyers.

31% of first-time buyers found the process “very/extremely stressful” versus 19% of repeat buyers.

66% of first-time buyers found it “at least somewhat stressful” compared to 56% of repeat buyers.

Homebuying stress

Total

Gen Z (Ages 18-30)

Millennial (Ages 31-45)

Gen X (Ages 46-60)

Boomers + Silent Gen (61+)

Very/extremely stressful

25%

30%

27%

25%

16%

At least somewhat stressful

60%

74%

64%

57%

48%

Not very/at all stressful

40%

26%

36%

43%

52%

Younger generations experienced higher levels of stress. Gen Z (Ages 18-30) and the 18-29 age group reported the highest percentages of “very/extremely stressful” (30% for both).

Stress levels generally decreased with age, with Boomers + Silent Gen (61+) experiencing the least stress (16% “very/extremely stressful” and 48% “at least somewhat stressful”).

Homebuying stress

Total

18-29

30-39

40-49

50-59

60+

Very/extremely stressful

25%

30%

28%

29%

22%

16%

At least somewhat stressful

60%

74%

65%

62%

55%

48%

Not very/at all stressful

40%

26%

35%

38%

45%

52%

Hispanic buyers reported the highest percentage of “very/extremely stressful” (31%) similar to AAPI buyers (26%).

Black buyers reported the lowest percentage of “very/extremely stressful” (19%).

AAPI buyers had the highest percentage of “at least somewhat stressful” (74%).

Nonwhite buyers collectively experienced slightly higher “at least somewhat stressful” levels (64%) compared to White buyers (59%).

Homebuying stress

Total

White

Black

Hispanic

AAPI

Nonwhite

Very/extremely stressful

25%

24%

19%

31%

26%

25%

At least somewhat stressful

60%

59%

55%

66%

74%

64%

Not very/at all stressful

40%

41%

45%

34%

26%

36%

Supplemental disaster insurance coverage

A slight majority of buyers (56%) reported purchasing supplemental disaster insurance coverage for at least one type of disaster in addition to their homeowner’s insurance policy, while 44% did not.

Most Common Coverage: Flood insurance is the most commonly purchased supplemental coverage overall (36% of buyers), followed by Tornado (23%), and Hurricane (22%).

First-time buyers are more likely to purchase supplemental disaster insurance across all categories compared to repeat buyers.

Notably, 33% of first-time buyers opted for no supplemental coverage, versus 52% of repeat buyers.

First-time buyers show higher percentages for Flood (43% vs. 31%), Tornado (28% vs. 18%), and Earthquake (23% vs. 16%) compared to repeat buyers.

Supplemental disaster insurance coverage

Total

First- time

Repeat

Earthquake

19%

23%

16%

Flood

36%

43%

31%

Hurricane

22%

25%

20%

Landslide

9%

12%

8%

Tornado

23%

28%

18%

Another disaster not listed above

5%

8%

4%

None of the above

44%

33%

52%

West: Shows significantly higher rates for Earthquake (36%) coverage, aligning with the prevalent natural disasters in the region.

South: Has the highest percentages for Flood (43%) and Hurricane (37%) coverage, consistent with common weather events in the area. Tornado coverage is also high in the South (28%).

Northeast: Shows moderate coverage for Flood (39%) and Landslide (12%), and relatively low for Hurricane (17%) and Tornado (17%).

Midwest: Has the lowest percentages for Flood (27%), Hurricane (6%), and Landslide (6%) coverage, but a notable percentage for Tornado (25%).

Supplemental disaster insurance coverage

Total

Midwest

Northeast

South

West

Earthquake

19%

14%

19%

12%

36%

Flood

36%

27%

39%

43%

34%

Hurricane

22%

6%

17%

37%

16%

Landslide

9%

6%

12%

9%

13%

Tornado

23%

25%

17%

28%

14%

Another disaster not listed above

5%

4%

3%

5%

9%

None of the above

44%

56%

49%

34%

46%

California: Stands out with extremely high earthquake coverage (55%) and high landslide coverage (18%).

Florida: Shows very high hurricane coverage (52%) and relatively high flood coverage (39%).

New York: Has high percentages for flood (47%), earthquake (36%), and tornado (34%) coverage.

Texas: Also shows high flood (47%) and hurricane (29%) coverage, along with significant tornado coverage (27%).

Supplemental disaster insurance coverage

Total

California

Florida

New York

Texas

Other

Earthquake

19%

55%

9%

36%

11%

15%

Flood

36%

34%

39%

47%

47%

34%

Hurricane

21%

16%

52%

27%

29%

18%

Landslide

9%

18%

6%

24%

8%

8%

Tornado

23%

17%

15%

34%

27%

24%

Another disaster not listed above

6%

7%

4%

6%

4%

6%

None of the above

44%

31%

30%

36%

31%

49%

Buyers who used cash were slightly more likely to have no supplemental coverage (50%) compared to mortgage buyers (42%).

Supplemental disaster insurance coverage

Total

Cash

Mortgage

Earthquake

19%

20%

19%

Flood

36%

31%

38%

Hurricane

22%

21%

22%

Landslide

9%

10%

9%

Tornado

23%

19%

24%

Another disaster not listed above

5%

5%

6%

None of the above

44%

50%

42%

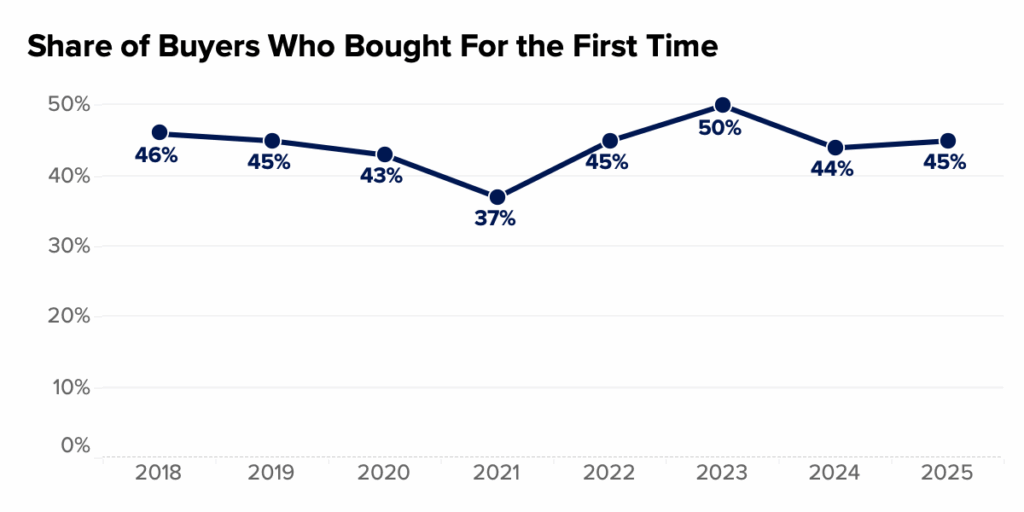

Share of First-Time Buyers

In 2025, the share of buyers who reported purchasing for the first time rose to 45%.

Share of Buyers that Bought For the First Time

2018

2019

2020

2021

2022

2023

2024

2025

46%

45%

43%

37%

45%

50%

44%

45%

The Homebuying Process

Time spent searching

Home search duration

Less than 1 month

11%

1 to less than 2 months

18%

2 to less than 3 months

19%

3 to less than 4 months

15%

4 to less than 6 months

15%

6 months or more

22%

Median

3-4 months

Cobuying is the norm, especially for partnered buyers

Most buyers (60%) purchase and share ownership of their home with at least one other person. Half of buyers (51%) cobought with a partner or spouse. Cobuying with a relative (8%) and/or friend (5%) was less common.

Cobought with

Feb- April 2022

Dec 2022

2023

2024

2025

Spouse/partner

45%

60%

50%

52%

51%

Friend

10%

4%

14%

7%

5%

Relative

11%

6%

12%

9%

8%

NET: Friend/relative

18%

8%

21%

15%

12%

Any cobuy

58%

65%

62%

63%

60%

Did not cobuy

42%

35%

38%

37%

40%

Most married or partnered buyers cobuy (75%) – most with a spouse or partner (68%). Buyers who are single and never married are most likely to cobuy with a friend or relative (18%, versus 9% of divorced/separated/widowed and 10% of married/partnered buyers).

One offer is typical for buyers — a slight decline from the past 2 years

The typical (median) buyer this year reported submitting one offer.

2018

2019

2020

2021

2022

2023

2024

2025

0 Offers

10%

11%

9%

6%

5%

8%

9%

10%

1 Offer

52%

49%

48%

36%

39%

38%

46%

47%

2 Offers

23%

23%

23%

28%

27%

27%

27%

26%

3 Offers

8%

10%

10%

18%

16%

16%

12%

12%

4 Offers

3%

3%

3%

7%

6%

5%

4%

3%

5 or More Offers

4%

4%

7%

6%

6%

5%

2%

2%

Median number of offers

1

1

1

1

2

2

1

1

Inspection, financing among most common offer contingencies

About two thirds of buyers (65%) say their final offer was contingent on the property passing a home inspection. Over half (59%) said the same about successfully receiving financing (e.g. mortgage approval). Contingency on the property appraising at a minimum amount was similarly common (53%). A mortgage rate buydown – where the seller agrees to buy down the buyer’s interest rate – was the least common: About a quarter of buyers (22%) said they won such a concession in their final offer.

Share of buyers that report including each contingency in their final offer

2022

2023

2024

2025

Financing

61%

61%

56%

59%

Appraisal

59%

58%

52%

53%

Inspection

70%

67%

66%

65%

Sale of my previous home recoded

29%

26%

23%

21%

Mortgage buydown

32%

24%

22%

Insurance (new in 2025)

53%

At least 1 contingency

85%

82%

82%

85%

Despite challenges and competition, buyers hold strong on inspections

Consistent with past years, buyers surveyed in 2025 did not budge when it came to forgoing inspections: Relatively few (14%) said that they did not get any inspections prior to purchasing their home.

2018

2019

2020

2021

2022

2023

2024

2025

0 inspections – I did not have any inspections conducted

15%

17%

18%

14%

13%

8%

17%

14%

1 inspection

60%

58%

53%

45%

53%

38%

54%

59%

2 inspections

16%

16%

16%

19%

17%

27%

18%

17%

3 inspections

5%

4%

6%

13%

10%

16%

9%

6%

4 inspections

1%

2%

2%

6%

4%

5%

2%

2%

5 inspections or more

2%

4%

6%

4%

3%

5%

1%

1%

Median inspections

1

1

1

1

1

2

1

1

Obtaining a pre-inspection report from the seller/builder is also quite common: Among buyers that remember, 64% said they got one, versus 36% who say they did not.

Among buyers that remember whether they got a pre-inspection report

2024

2025

Got pre-inspection report

66%

64%

No pre-inspection report

34%

36%

Among buyers that reported having no inspection of their own conducted, 37% reported getting a pre-inspection report. These no-inspection buyers were less likely to purchase a single-family detached house (59% versus 80%) and were more likely to buy a manufactured/mobile home (20% versus 5%) or a boat/RV/van/etc (5% versus 1%).

The Buyer-Agent Partnership

Buyers almost always use an agent

Most buyers reported using an agent among the resources they used to shop, search, or purchase their home (84%). Among buyers that used an agent, 75% say they hired their agent to help shop for and purchase their home. About a quarter (25%) hired an agent to finalize their home purchase, but shopped on their own.

Resource used during any part of searching, shopping for or purchasing their home

2019

2020

2021

2022

2023

2024

2025

Real estate agent, broker or realtor

82%

85%

82%

89%

88%

85%

84%

First-time buyers (83%) and repeat buyers (86%) report using an agent at similar rates.

Buyers without an agent more likely to buy low-cost homes

About a third (32%) of buyers that paid less than $100,000 for their home said they did not use an agent – higher than 16% of buyers overall.

Among buyers that did not use an agent, about a fifth purchased a manufactured or mobile home (19%) – versus only 2% among buyers who used an agent.

Already knowing their seller among top reasons for forgoing an agent

Among buyers that did not use an agent, almost half (48%) said they already knew the seller (45%) or purchased their home from someone they knew personally (41%) (like a friend, family member, or coworker).

Not wanting to pay a real estate agent’s commission (35%) was another common reason.

Websites, apps and referrals top resources where buyers find agents

First found agent

2018

2022

2023

2024

2025

Real estate website / app (e.g. Zillow, RE/MAX, Realtor.com)

16%

18%

25%

23%

22%

Referral from friend, relative, neighbor or colleague

27%

21%

18%

22%

20%

Know them from my community

7%

12%

6%

8%

11%

Past experience with this agent or broker

10%

8%

8%

8%

9%

Social networking website / app (e.g. Facebook, NextDoor, Twitter, Instagram)

2%

5%

8%

7%

5%

Search engine (e.g. Google, Bing)

5%

5%

7%

7%

6%

Saw contact information on For Sale/open house sign

7%

4%

5%

6%

5%

Attended an open house and met agent or broker

5%

5%

4%

5%

6%

Referral from another agent or broker

6%

7%

6%

5%

7%

Referral from home builder

2%

3%

5%

4%

3%

Direct mail (e.g. newsletter, flier, postcard)

2%

3%

3%

2%

2%

Newspaper ad

2%

1%

1%

1%

2%

Other

9%

8%

6%

3%

2%

Net: Online

23%

28%

40%

37%

33%

Net: Referral

35%

31%

28%

30%

30%

Survey Methodology

Research Approach

To gain a comprehensive understanding of the US homebuyers, Zillow Group Population Science conducted six nationally representative surveys – collecting over 57,600 responses (approximately 20,000 from successful buyers and 37,600 from prospective buyers). The survey contains information from approximately 10,200 unique successful buyers and 18,100 unique prospective buyers. The study was fielded between April and September 2025.

Wherever possible, survey questions from previous years were asked in the same manner this year to allow for the measurement of year-to-year trends in key areas of business interest.

For the purpose of this study, “successful buyers” – typically shortened to “buyers” refers to household decision makers 18 years of age or older who moved to a new primary residence that they purchased in the past two years. A majority of buyers in this sample (54% unweighted; 55% weighted) purchased within the past year.

Sampling & Weighting

Results from this survey are nationally representative of successful buyers. US adult decision makers were identified from online nonprobability samples. To achieve representativeness, we used a combination of quota sampling and statistical raking using benchmarks estimated from the 2023 American Community Survey (ACS) and the 2024 Current Population Survey Annual and Economic Supplement (CPS ASEC).

To ensure that this weighting procedure did not drive observed results, we created several alternative sets of weights for key estimates of interest. These alternative weights included several versions with additional population characteristics– especially those that could be correlated with estimates of interest– from external sources, as well as propensity matching to better capture a given respondent’s underlying probability of participating in the survey. None of the alternative sets of weights substantively shifted the estimates examined.

Quality Control

To reduce response bias, survey respondents did not know that Zillow Group was conducting the survey. Several additional quality control measures were also taken to ensure data accuracy:

We identified and terminated any professional respondents, robots or those taking the survey on multiple devices.

Completion times were recorded to ensure that surveys submitted by the fastest respondents, who may have rushed through the survey, did not provide poor quality data. If necessary, these respondents were removed from the sample.

In-survey quality control checks identified illogical or unrealistic responses.

[1] Zillow Group Population Science defines Gen Z as those born between 1995 and 2003, Millennials between 1980 and 1994, Gen X between 1965 and 1979, Baby Boomers between 1945 and 1964, and Silent Generation in 1944 and earlier.

[2] LGBTQ+ buyers are those who identified as gay, lesbian, bisexual, transgender, gender non-conforming/non-binary, intersex, or with another sexual orientation (other than straight) or gender identity (e.g. gender fluid, gender queer, gender neutral).

[3] Median household incomes are from Census Bureau, 2023 Current Population Survey Annual Social and Economic Supplement.

[4] These estimates come from CHTR 2023 and the 2019 American Community Survey.

[5] The estimated share of all households with pets comes from American Housing Survey (AHS) 2021. These numbers are likely systematically low because of rising pet ownership following the COVID-19 pandemic. AHS also excludes service animals and livestock from their survey definition, whereas CHTR does not specify exclusions for any animals/pets.

Tenured homeowner household pet estimates come from CHTR 2021 (the last year CHTR included tenured homeowners) while buyer estimates are from CHTR 2023.

[6] The estimated shares of households (buyer, tenured homeowner, and all households) with children comes from the 2023 Current Population Survey Annual Social and Economic Supplement.

[7] This survey defines “cobuying” as sharing ownership of the home with at least one other person. While more than 71% of married/partnered buyers likely reside with or involve their spouse or partner in their home purchase, 71% is the share who self-report sharing ownership of the home with their spouse/partner.

The post Buyers: Results from the Zillow Consumer Housing Trends Report 2025 appeared first on Zillow Research.